Ag Markets and Trade: A Conversation about the Uncertainty

Author

Published

4/12/2018

Eric Wilkey is president of Arizona Grain, Inc., having joined the company in 1991. From 1996 until 2006 he was vice president and director of merchandising and risk management.

Before moving to Arizona and joining Arizona Grain, Inc., Wilkey worked for six years with Continental Grain Co. in various locations throughout North America as a product line Commodity Merchandiser.

He currently serves as the Chairman of the National Grain and Feed Association, with past service as the chairman of NGFA’s Grain and Feed Foundation as well as chairman of the Transportation Grain Merchants Association. Since 2004, he has served the State of Arizona by appointment of Governor Ducey and his two predecessors as a member of the Arizona Grain Research and Promotion Council, serving as chairman in 2006-2007.

Wilkey is a graduate of the University of Illinois, Champaign, with a B.S. in Agriculture Economics.

Coaching the High School Mountain bike team in Casa Grande for three high schools since 2013,

Wilkey finds mountain biking a healthy and fun break from the crazy commodity markets

but with still a touch of risk and adventure to keep him challenged.

Outside of work Wilkey is a registered coach with the National Interscholastic Cycling Association and has coached the High School Mountain bike team comprised of students for Casa Grande, Arizona three high schools from the inaugural year in 2013 to present.

Having stayed in touch with Wilkey over the years in part because of his wise insights on commodity markets, he had some interesting opinions on recent trade moves and certain concerns about how our current administration plans to promote infrastructure efforts in America’s rural areas. Here is our latest conversation.

Arizona Agriculture: Give us an overview of how you see the market in the next few months.

Wilkey: Since my experience is in commodity markets, specifically grain, oilseed and protein markets I will give my thoughts on those areas. In general, the price levels in these markets have been

That could be changing. If the change is real then should the grain and oilseed, fiber and forage producer get ready for better times? Should the animal sector, who benefit from the lower price inputs, brace for a rally? I’m not so sure, here is why. The past six months it has been difficult to see how commodity prices in the U.S. would rise enough to qualify as a rally. It has been an educated guess that it would take a significant negative weather trend in one of the world’s major production hubs to tighten the World supply surplus before a significant and sustainable rally could take place. Plain and simple, the surplus of many commodities is too large.

That may be changing. The past four months, we have witnessed the stability of South American soy production put into question and a significant drought has hit Argentina. The losses are real. The big question is will Brazil, who’s soy production areas have had more favorable weather, make up for the certain losses in Argentina? This uncertainty has provided a spark. Will it turn into something significant for the market? Still a bit early to tell. What we can tell is that it has touched off volatility.

Other production concerns are the western Great Plains hard wheat areas. Drought indications have been increasing and this could be a second major crop area with production challenges. This has generated a stronger and more volatile wheat market in the past few weeks.

But before we know the rally is at hand the U.S. markets face BIG headwinds from a whole host of exogenous factors: Trade policy, lack of a breakthrough on the renegotiation of NAFTA, questions about Korea Free Trade Agreement (KORUS) status, lack of any progress of any bilateral trade agreements, abandonment of the TPP trade negotiations (the completion of the agreement and signing in Santiago, Chile on March 8, 2018), and now the imminent threat of steel and aluminum import tariffs. These factors are trending negatively for the agriculture sector and mere tighter supply and demand tables will not offset the impact of dollar volatility and negative trade developments.

The issue is clear, to me there is more uncertainty in market structure and trade policy than we have had in years and if a lack of reasonable certainty exists it is hard to imagine that the supply and demand tables hold the key drivers to future price direction. To me, this means volatility, more day-to-day chatter in prices with less predictable patterns that we can rely on to make informed buying and selling decisions. Market and risk management plans that focus on margin management should rule buyer’s and seller’s decisions.

Arizona Agriculture: In an earlier interview I had with you this year, you outlined ways to improve our agriculture commodity markets. Can you share in more detail here?

Wilkey: Two factors that I pointed out in recent statements are the need to improve competition in transportation and the need for fair and free or at least trade that is not impeded by excessive or unreasonably protective tariffs, or maybe worse yet non-tariff trade barriers.

More on the trade first. We in agriculture have a pretty strong appreciation for the positive benefits of trade. We cannot look for prosperity unless we have access to outside markets that are willing to buy our surpluses. We simply are too productive and do not have enough consumers within our own borders to go without exports. Trade results in an allocation of labor and resources, this takes time. After 20 years of NAFTA that change has happened, somewhat gradually, and predictably. What is being talked about and or implemented now will not result in a gradual allocation of resources towards the benefits of comparative advantage. There are plenty of voices making the point how badly we need to be part of healthy trade agreements yet other than hanging on by our nails in the NFTA talks it remains difficult to see this need is resonating with the current administration. Not enough credit can be given to Agriculture Secretary Perdue for his herculean efforts of keeping us in the NAFTA discussions and maintaining the KORUS Agreement. So, unless there is a darn perfect grand strategy being played out, one I admit that I cannot fathom, then it seems the forecast for agriculture looks rather discouraging.

The other part of my suggestions for improving

Arizona Agriculture: On that point, your solution for improving our rural and transportation infrastructure has merit. You’ve seen what Trump has proposed. Is it enough? What else would you suggest?

Wilkey: The infrastructure proposals by the Trump administration sound grand but the amount of spending is very highly leveraged using State, Local and private funds to make up most of the spending. This calls into question the amount that will actually be spent in a meaningful time period. Rural areas are supposed to get priority but the devil is in the detail.

I am not in favor of relying too heavily on private ‘investments” in roads and infrastructure as the underlying motivation for profits and the direct need to generate investable returns places a toll on the project that in the end means the projects have a higher cost on the users. There are projects that this model may be acceptable but this should not be the primary basis of our future road and infrastructure building.

The country needs to come to grips with the reality that the current Federal and State fuel taxes do not keep up with the maintenance and expansion of our transportation infrastructure. Federal fuel tax rates have not changed since 1993 and many states have not changed their rates either. While total miles driven have continued to rise, the increased fuel efficiency requirements and the use of EV’s and some alternative fuels will mean there will be a flattening or even a decline in the funds that are collected for road repair and building. This needs to be addressed. There will need to be consideration given to how to charge the growing number of users of EV and certain other fuel technology vehicles pay their fair share of the road and infrastructure costs.

Federal infrastructure projects that have funding but are held up by never-ending analysis and litigation need to be priorities for progress. The lock and dam systems have billions in barge fuel taxes paid by the industry that has not been put to work yet. Our Ag export capabilities are hamstrung with a lock and dam system that is decades beyond its original service life. This also prevents viable competition to railroads and burdens the road systems with freight and increases a less efficient means of transporting goods to limit ag products to export markets.

The Trump proposal calls for block grants to States and the money would be doled out partly based on a yet to be defined “rural lane miles” formula. Trouble is the Federal government has many definitions of “rural.” Any infrastructure plan should consider how rural areas have access to information. Trump’s proposal lacks this vital link, this is a mistake. Maybe the Farm bill will include funding for this. It needs to be there if we want farms and U.S. ag to keep up with the competition.

Arizona Agriculture: Talk about our opportunities in global markets. Knowing that we’re out of the TPP and waiting on NAFTA, what can we do despite these tenuous trade relations?

Arizona Agriculture: Make comparisons with the West’s grain market compared to the Midwest. What do we do well out here in the West?

Wilkey: The biggest difference in the West’s grain markets versus the Midwest is the price structure. The West tends to have higher prices versus the Midwest which is a result of transportation cost from the surplus markets to the West and the impact of water costs on production. The West (I’m thinking west of the Rockies) is relatively small in terms of grain production. The western farmer is a capable producer of grain but the production of grain has declined partly because of changes to the price support programs in the past few farm bills, which overall has led to a better allocation of resources. However, the consumers of grain in the west, the livestock producer, dairy farmer and egg producer has become vulnerable to the pricing power of the railroads which currently have no effective competition and little outside restriction to their margin expansion. The western farmer has shown that they are very adaptable with many farms capable of producing and marketing many more crops than their Midwestern counterpart. Clearly, the western producer excels in water management, adapting to the change in the farm programs and to the shifts in world production centers.

Arizona Agriculture: Our new Chairman of the Federal Reserve talked about a strong dollar. This can hurt agriculture. Talk about this?

Wilkey: A strong dollar can hurt agriculture exports without a doubt but maybe it’s a strengthening or volatile dollar that hurts agriculture even more. The strong dollar makes imports cheaper in dollar terms and our exports less attractive. It may be tempting to advocate for a weaker dollar at times but I see more advantages when it comes to the allocation of resources to have stable values. Weak currencies lead to inflation and inflation leads to real problems in commodity production.

Arizona Agriculture: Handing you the crystal ball, what’s your take on our future?

Wilkey: My last comment is to make the point that U.S. agriculture needs to work from its and our common positions. Our industry associations and advocacy groups deliver value to their members and we compete in agriculture for members of our groups. There are positions on issues that we may not have

There will be fewer farmers and companies (continued consolidation) that are engaged in production agriculture. There will be continued consolidation of which leads to a consolidation of dollars and possibly a more self-interested focus. We will have less electorate clout on the political front to sustain ourselves so we must be more strategic within our industry. We need leaders who see the merit of working together whenever we can.

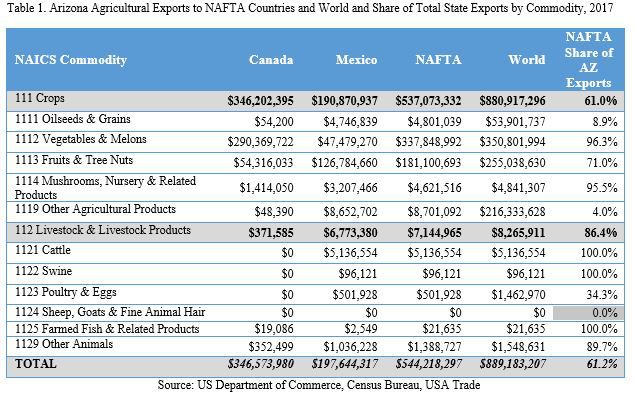

Editor's note: At $23.3 billion, Arizona’s agriculture makes a significant impact on our state. Related to just trade, last year, 61% of Arizona’s agricultural exports of $889 million were purchased by NAFTA trading partners: $346 million (39%) by Canada and more than $197 million (22%) by Mexico. Arizona’s crop exports to NAFTA partner countries has grown since the agreement’s implementation in 1994. From 2002 to 2010, the value of crop exports nearly doubled, to over $600 million in 2017 U.S. dollars. That figure has since fallen and stabilized to around $500 million annually, according to Ashley

Their report further states: "According to Commerce data, Canada is a primary destination for Arizona crop exports, while Mexico is a major destination of Arizona livestock exports. Table 1 nearby lists major agricultural commodities according to their North American Industrial Classification System (NAICS) code. The export figure for Fruits and Tree Nuts is overstated because it includes products such as apples and pears, not widely grown in Arizona, but that are consolidated there for shipment to Mexico. The export figure also understates vegetable and melon sales to Canada. For example, from December through February, Arizona produces 80% or more of all U.S. lettuce. Yet, for these months, Arizona accounts for less than 40% of lettuce exports to Canada, while a sizeable share of exports